But what you do NEXT does.

We help people just like you remove inaccurate items, boost scores, and give you a clear path forward - without the guesswork.

But what you do NEXT does.

We help people just like you remove inaccurate items, boost scores, and give you a clear path forward - without the guesswork.

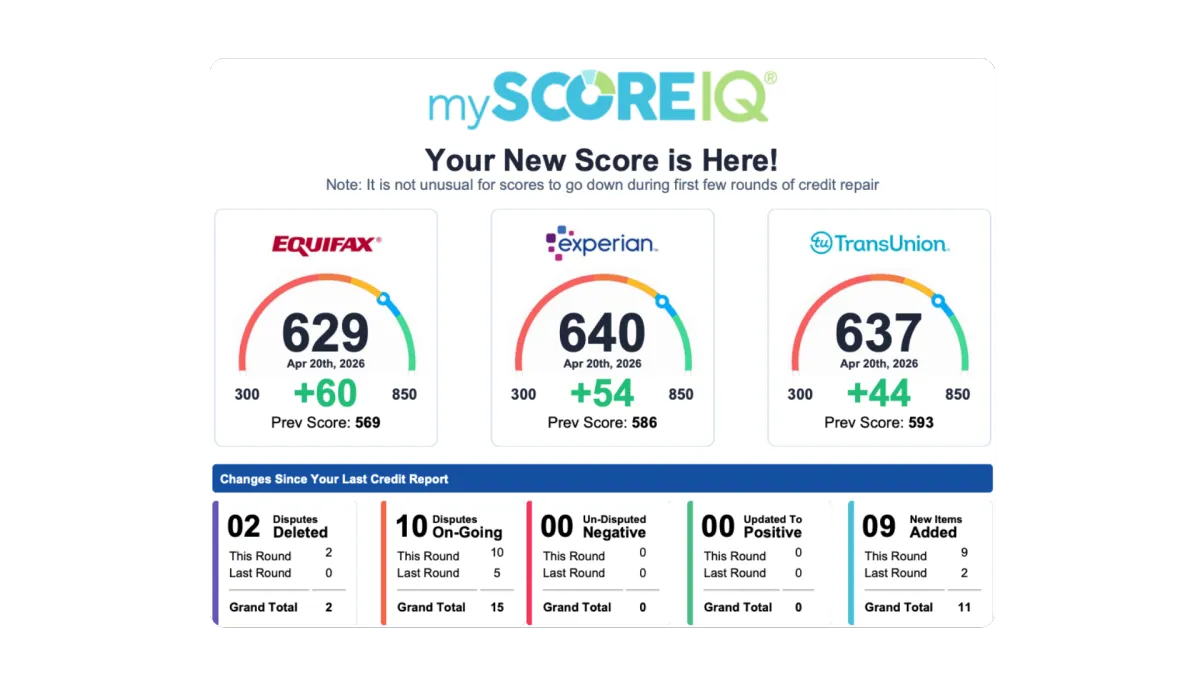

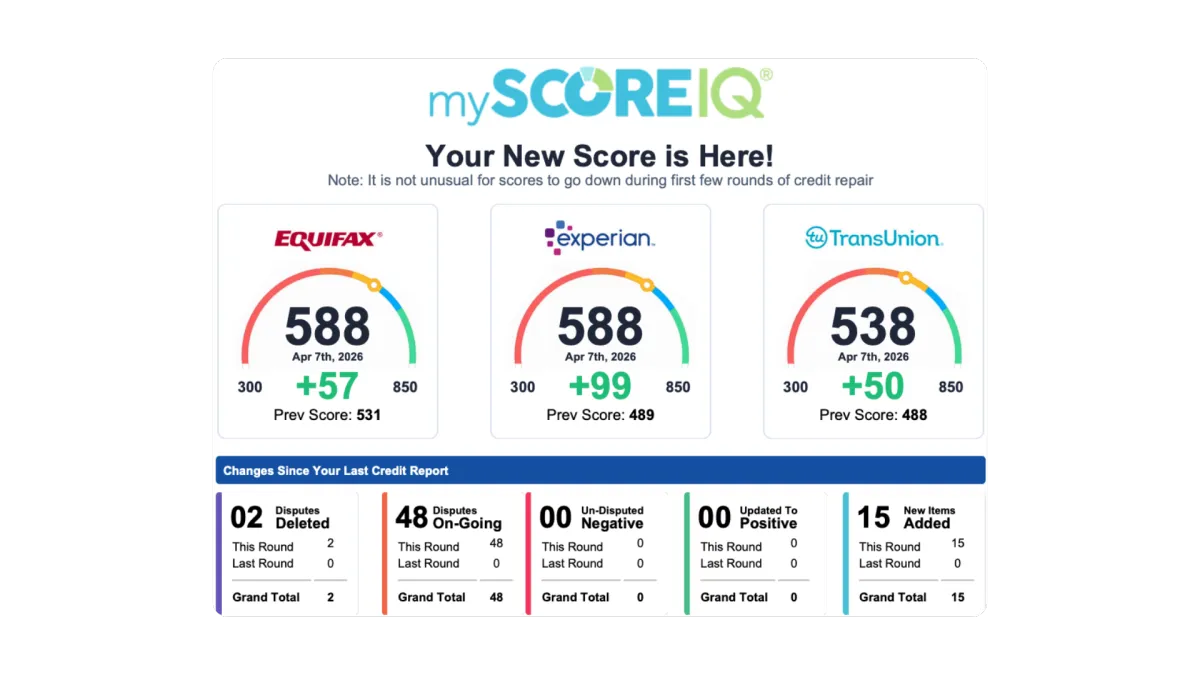

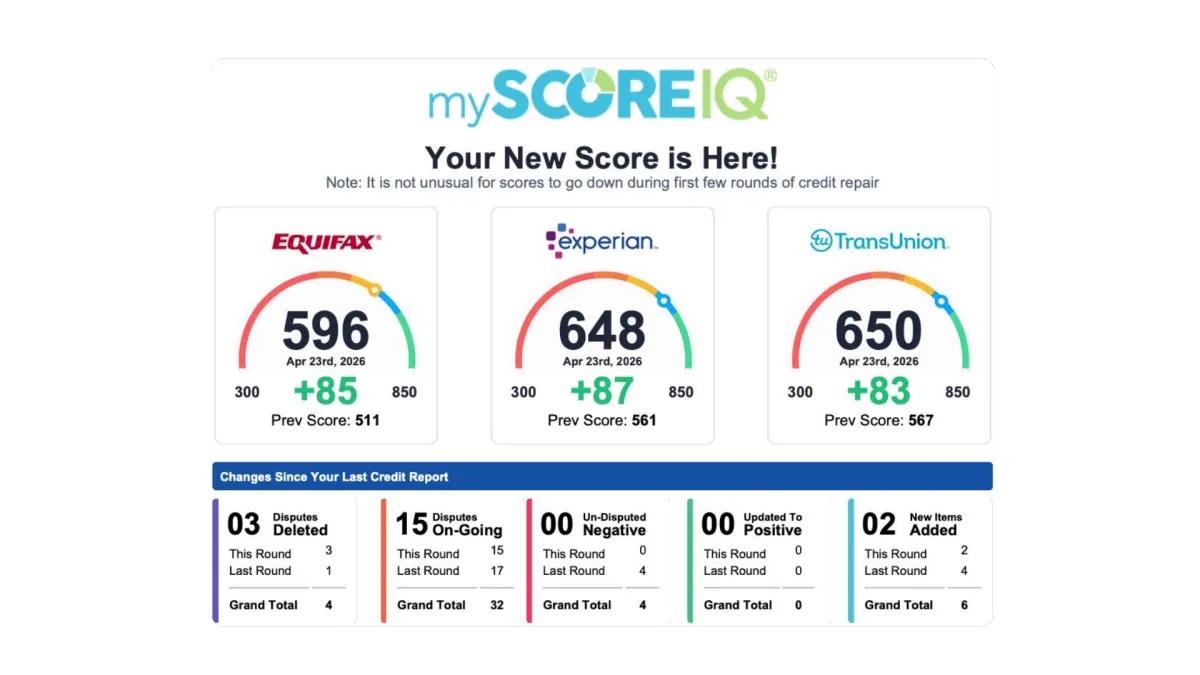

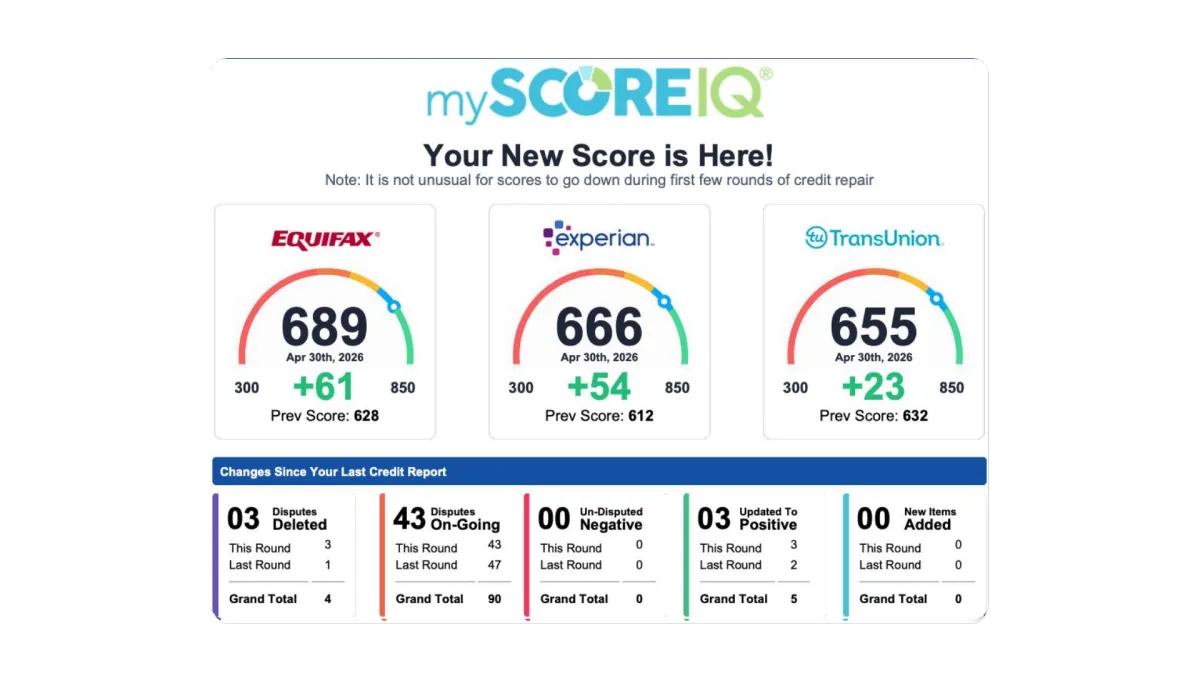

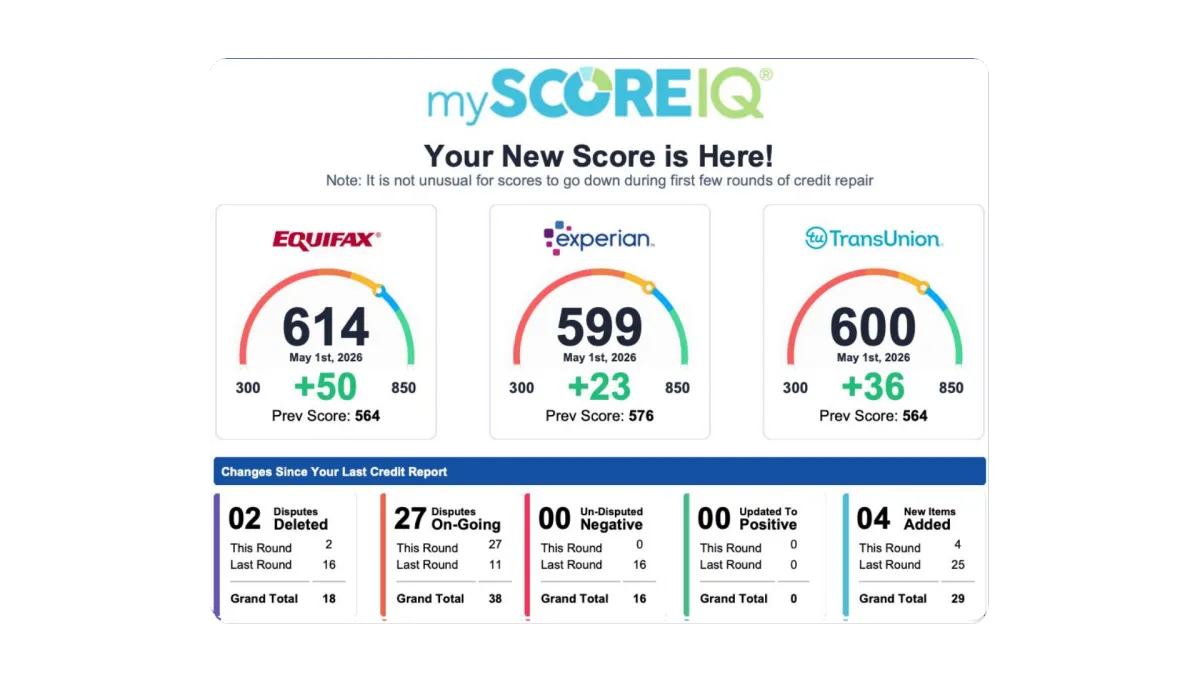

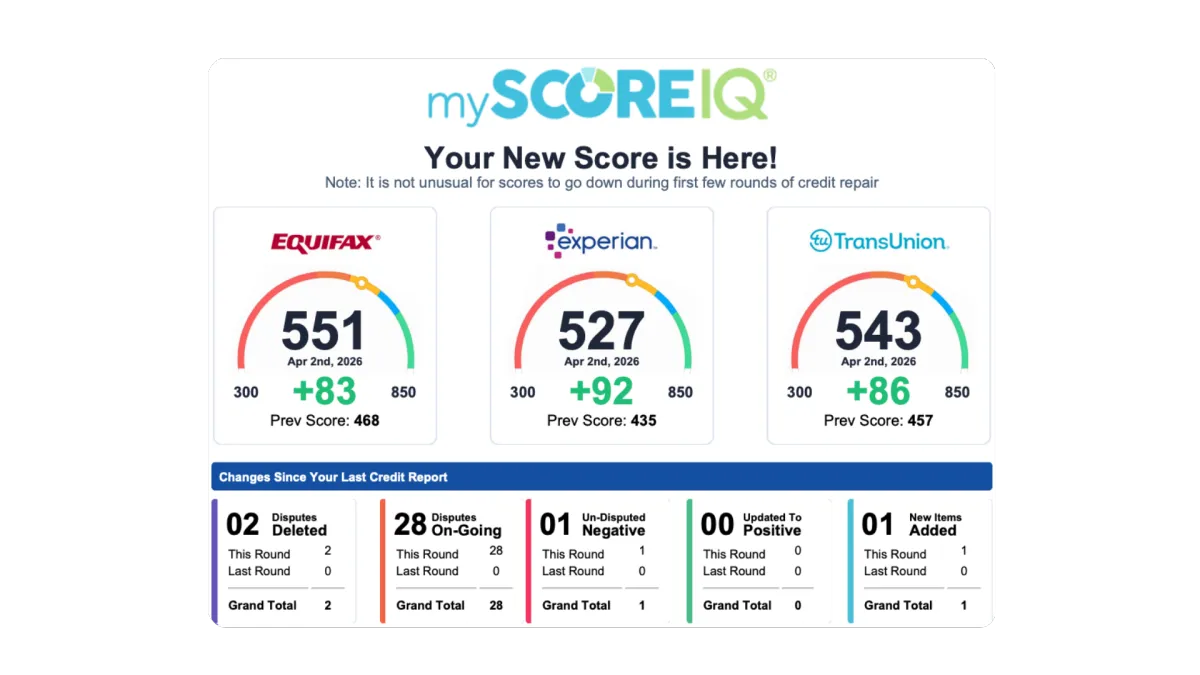

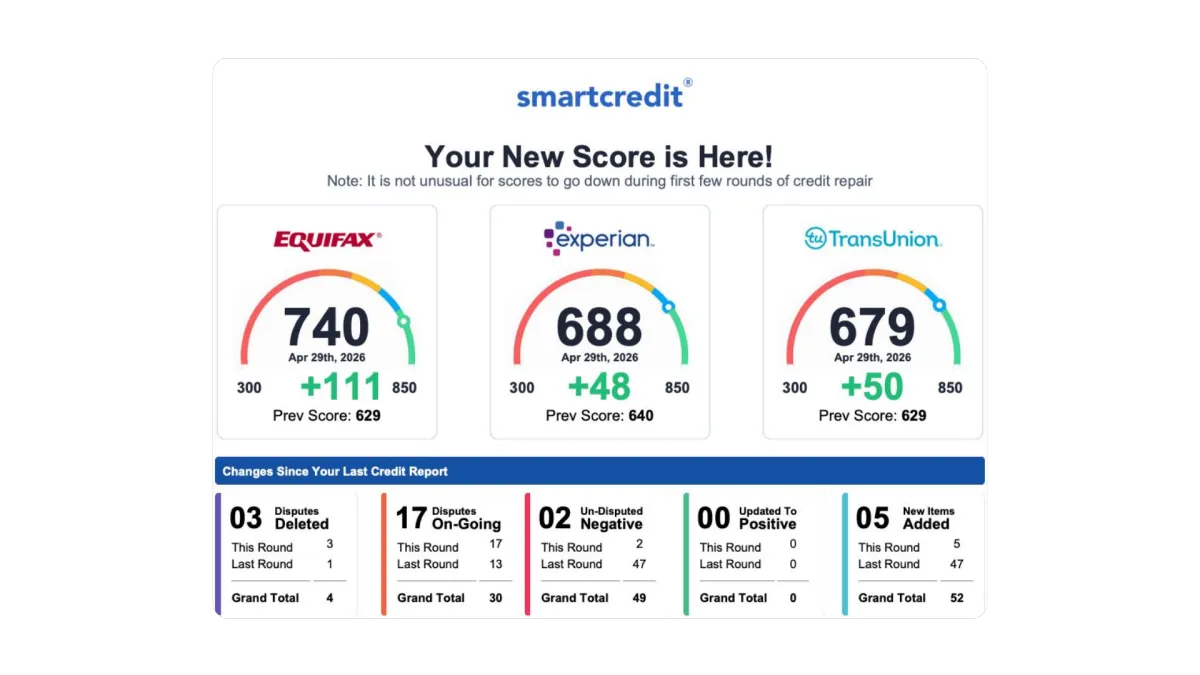

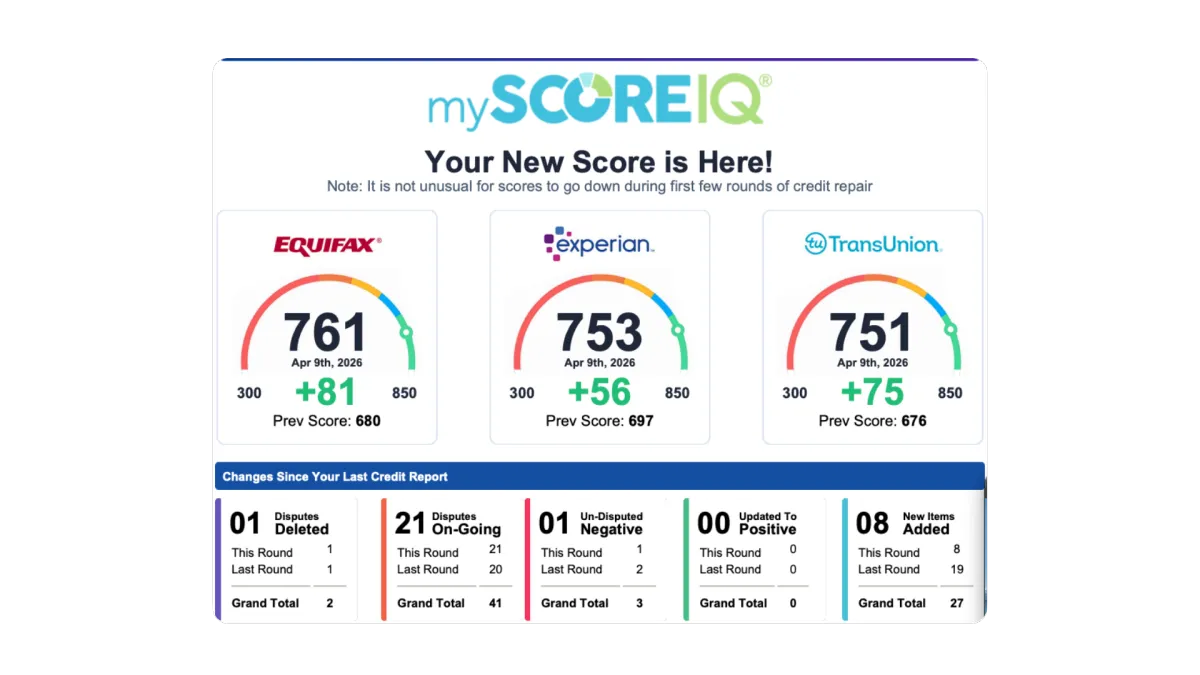

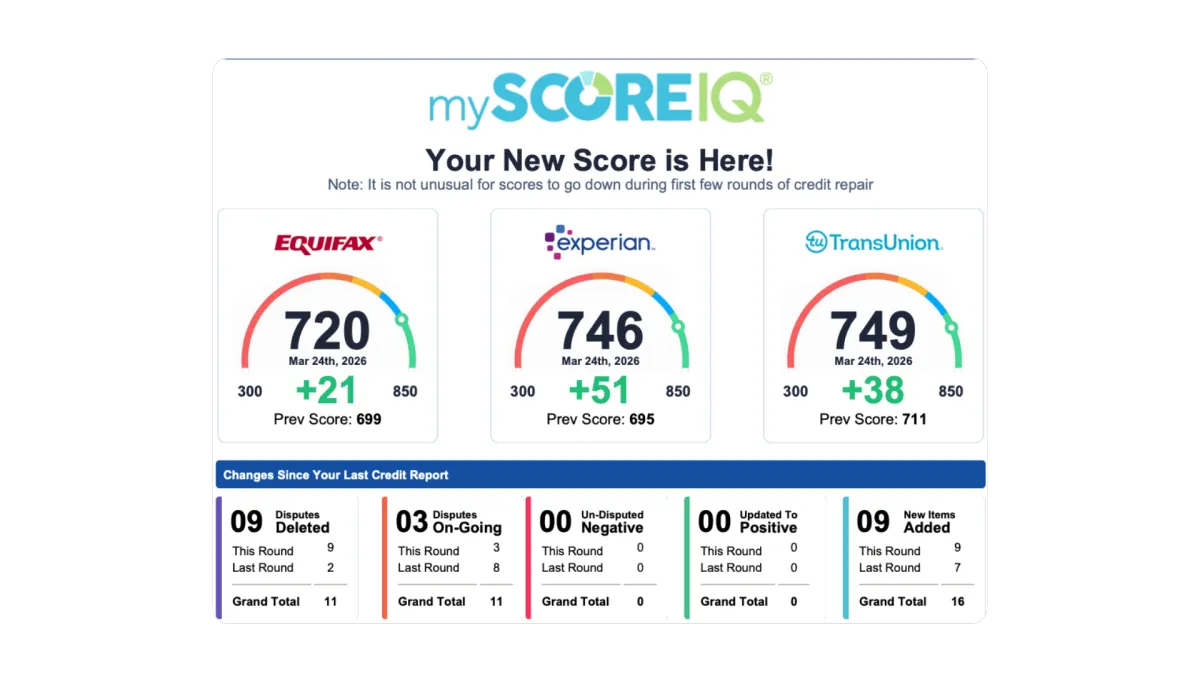

PROVEN RESULTS. REAL IMPACT.

SEE HOW WE TURN NEGATIVE CREDIT INTO NEW OPPORTUNITIES.

HOW WE HELP YOU

WE AUDIT

We review your full credit reports and identify inaccurate or negative items.

WE CHALLENGE

We dispute inaccurate, unverifiable, and outdated information with creditors.

WE IMPROVE

We work to remove negative items and help improve your credit over time.

WE SUPPORT

We guide you every step of the way with ongoing support and updates.

WHAT OUR CLIENTS SAY

DON'T WAIT TO FIX YOUR CREDIT

SEE IF YOU QUALIFY NOW

DON'T WAIT TO

FIX YOUR CREDIT

SEE IF YOU

QUALIFY NOW

It only takes 2 minutes to get started. Limited free consultations available this week.

Have questions before getting started?

Scan to text Next Step Credit Repair.

TRUSTED. CERTIFIED. PROVEN.

FREQUENTLY ASKED QUESTIONS

When is the best time to start your service?

Yesterday!

That answer really depends on your personal goals. Whatever your personal credit and financial goals are, it’s important to remember that credit repair is not an overnight “quick-fix” and takes time. Many people can start to see an increase in their score in as little as 30 days but the process of going from bad credit to good credit typically takes much longer. Your score didn’t get bad overnight and it doesn’t improve that way either.

Why is credit so important?

Your credit can affect your ability to get approved for things like a car, home, apartment, credit card, or loan.

Better credit may give you better approval chances and better rates. That’s why it’s important to understand and take care of it.

How much does credit repair cost?

Make no mistake-bad credit comes at a cost. Credit affects every area of your life, from your ability to buy a house to the way potential employers view your application. Those living with bad credit understand the disputes it causes.

How long does it take to fix bad credit?

There is no fast and easy answer to this question. The time it takes to repair your credit is completely dependent upon your personal situation.

How do we communicate with you?

We are here for you throughout your credit-repair experience. You can always email us with any questions you have.

We’ll get back to you promptly so that you can always keep moving forward.

What are the 3 credit bureaus?

The three major credit bureaus are Equifax, Experian, and TransUnion.

These companies collect information about your credit history and create credit reports that lenders may use when reviewing applications for loans, credit cards, housing, or other financial decisions.

Because each bureau may have slightly different information, it’s a good idea to review all three reports so you can spot errors and understand what may be affecting your credit.

How is my credit score calculated?

Your credit score is made up of a few different factors, but don’t worry, we’ll keep it simple:

The biggest part is your payment history, which means whether you pay your bills on time. That makes up about 35% of your score.

The next big factor is how much you owe, which makes up about 30%.

Other things matter too, like how long you’ve had credit, the types of accounts you have, and whether you’ve opened new accounts recently.

Your score usually ranges from 300 to 850. The higher your score, the better you may look to lenders.

Our goal is to help you understand what’s affecting your score and what steps may help improve it over time.

YOU DON'T HAVE TO STAY STUCK

YOU DON'T HAVE TO

STAY STUCK